KEY POINTS

- Bitcoin passed $63,600 at one point on Sunday night before holding at the $63,000 lows early Monday

- Other coins were also up, including ETH, BNB, and Solana’s SOL following positive news last week

- Some observers expect BTC to come in ‘strong’ this month due to the coin’s historical patterns

Bitcoin opened the week strong after the world’s largest cryptocurrency by market value climbed from the $61,000 lows to $63,000 over the weekend, marking the end of the digital coin’s weeks-long struggle near the $60,000 line.

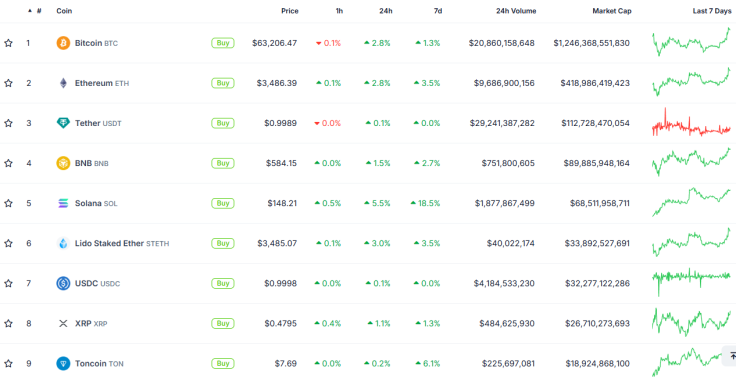

The world’s top digital asset ended the weekend in the green, at one point passing $63,600, as per data from CoinGecko. It settled at around $63,200 early Monday, and has been up by over 2% in the last 24 hours.

CoinGecko

Bitcoin’s recovery seems to have pulled up other top coins too. Ethereum ($ETH) has been up by 2.8% in the last 24 hours and lodged a 3.5% spike in the past week. Binance Coin ($BNB) increased by 1.5% and Lido Staked Ether ($STETH) climbed by 3%.

Solana ($SOL) lodged the largest 7-day gains, rising by over 18% in the past week and spiking by 5.5% in the past 24 hours.

CoinGecko

It is worth noting that the $SOL token’s significant weeklong rally came in the background of VanEck’s filing with the SEC late last week to issue the United States’ first potential spot Solana exchange-traded fund (ETF).

The cryptocurrency community on X (formerly Twitter) reacted positively to the news that $BTC is on the road to recovery and may have finally ended its slump season.

“Historically, July has been a positive month for Bitcoin recovery, often following a declining June,” wrote crypto enthusiast Tomi Point. He noted the same pattern in July 2020, when the digital currency surged by 24.03%.

🚀 #Bitcoin is on the rise, climbing nearly 4% today! 📈

Starting July strong, Bitcoin’s price stands at $63,277.83, marking a 3.76% increase. This recovery is a welcome surprise after June’s 6.96% drop. Historically, July has been a positive month for Bitcoin recovery, often… pic.twitter.com/Z9qXyT1yJ0

— Tomi Point (@tomipoint) July 1, 2024

Crypto analyst Ali Martinez agreed, saying that $BTC has had a “negative June” in past cycles, but the coin “tends to bounce back strongly in July.”

While hopes are high about Bitcoin being poised for a strong comeback this month, there are still concerns about the MtGox dump this week that the collapsed crypto titan previously announced.

MtGox, which filed for bankruptcy in 2014 after it lost around 750,000 $BTC owned by its users and some 100,000 of its own Bitcoin stash, announced last week that it will start repaying customers “from the beginning of July 2024.” MtGox is expected to make up to $9 billion in repayments.

Ahead of the repayments, a digital wallet linked by blockchain analytics firm Arkham Intelligence to MtGox, moved some $10 billion worth of Bitcoins within a period of seven hours in May. The transfer rocked the Bitcoin community, but the fallen exchange’s former CEO said the move was likely made in preparation for the repayments.

It remains to be seen how $BTC will be affected by the upcoming massive dump, but for now, the digital coin is on the uptrend.

{kind=link}