Reuters

Japan’s new central bank Governor Kazuo Ueda gave a clear message to policymakers gathered for global finance meetings here over the last week: The country will remain a dovish outlier by keeping interest rates ultra-low – at least for now.

Since taking the helm a week ago, Ueda has dropped some hints the massive stimulus of his dovish predecessor Haruhiko Kuroda will eventually be phased out.

But discussions over when and how to shift away from the ultra-loose policy will take time, giving Ueda every reason to reassure the world any change won’t happen quickly.

“In many countries, inflation is very high or not slowing enough. The important thing is that the situation is quite different in Japan, which I explained at the meeting,” Ueda told reporters on Wednesday after attending a finance leaders’ meeting of the Group of Seven advanced economies, held alongside the spring meetings of the International Monetary Fund and World Bank.

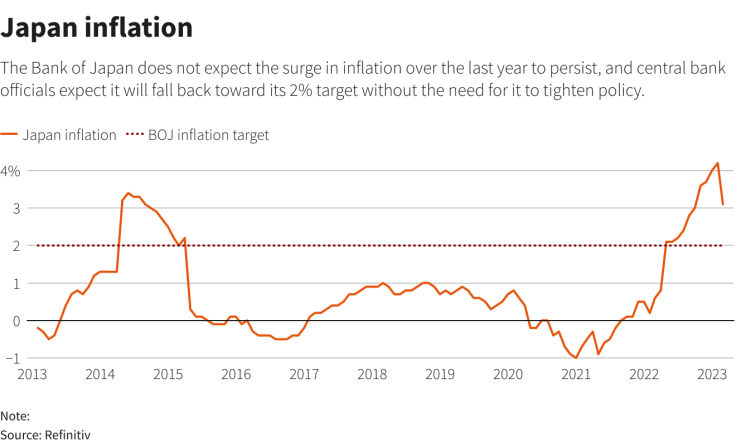

Japan’s inflation, now around 3%, will slow back below the BOJ’s 2% target later this year on falling import costs, Ueda told Thursday’s bigger gathering of ministers from the Group of 20, in explaining his plan to keep monetary policy ultra-loose for now.

The dovish remarks likely underscore the BOJ’s desire to avoid a repeat of January, when markets anticipating a swifter pivot by the BOJ to tweak to its yield curve control (YCC) policy pushed up long-term interest rates.

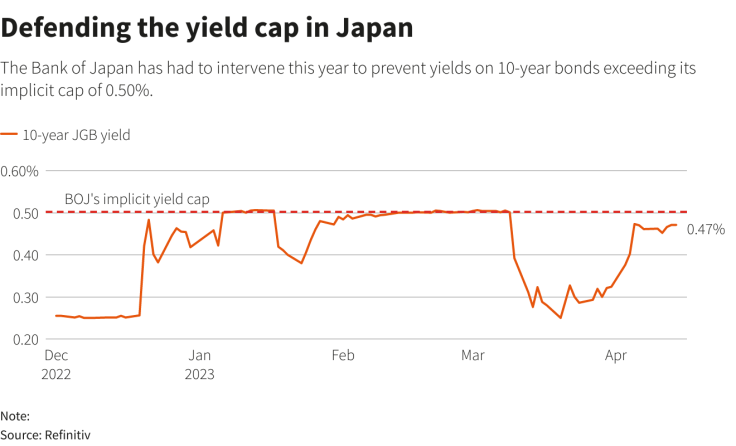

Under YCC, the BOJ guides short-term rates at -0.1% and the 10-year Japan government bond yield around zero with an implicit cap of 0.5%. With inflation exceeding the BOJ’s target and the cost of prolonged easing increasing, markets are rife with speculation that Ueda will move towards tweaking YCC this year.

The 10-year yield is currently a shade below the cap at 0.47%, but on repeated occasions earlier this year traders drove it above 0.5%, pressing the BOJ to defend the mark.

GRAPHIC: Defending the yield cap in Japan (

)

SCOPE TO TWEAK THIS YEAR

Ueda will chair his first BOJ policy meeting on April 27-28, when the board will issue fresh quarterly growth and inflation forecasts that will come under scrutiny for signs on how soon the central bank projects inflation to sustainably hit its 2% target.

Uncertainty over the world economy, highlighted by the International Monetary Fund’s stark warning of global recession risks on Tuesday, adds reasons for Ueda to move slowly and cautiously.

And yet, analysts say Ueda’s remarks leave scope for changes to YCC, which has drawn criticism for distorting the shape of the JGB yield curve and crushing financial institutions’ margin.

While stressing that the BOJ’s focus now should be to avoid a premature exit, Ueda said on Wednesday he won’t deny the risk of being behind the curve in addressing too-high inflation.

That followed his remarks on April 10 that the BOJ must make “pre-emptive” decisions on the timing of normalizing policy, as waiting too long could make the adjustment disruptive.

“We’ll discuss all options at each of our policy meetings,” Ueda said on Monday, when asked about the chance of adjusting the BOJ’s guidance committing to keep interest rates ultra-low.

“Ueda and his deputies are taking care not to give any hint on the timing of a policy tweak,” said former BOJ official Nobuyasu Atago, currently an analyst at Ichiyoshi Securities.

“But they also haven’t completely ruled out the chance of a near-term tweak to YCC,” he said.

GRAPHIC: Japan inflation (

)

SUPPLY SHOCKS, TRADE OFFS

Intensifying global debate over the cost of delaying monetary tightening could challenge the BOJ’s view the recent cost-driven inflation will prove temporary.

IMF First Deputy Managing Director Gita Gopinath said the days when central banks could focus on demand, and assume that supply would be elastic and a given, may be over.

“We’re in an economy where we’re going to be hit more by supply shocks, and monetary policy will face more serious trade-offs,” she said on Friday.

The IMF had a piece of advise to Ueda: relax the BOJ’s control and allow long-term rates to rise more flexibly – a move that will help ease the strain on the banking sector.

Ranil Salgado, the IMF’s Japan mission chief, sees scope for the BOJ to modify the long-term yield target this year, given heightening prospects of durable wage growth.

As long as the short-term rates remain zero or slightly negative, the BOJ can keep monetary policy accommodative even if it tweaks the yield target, he said.

“We are advising (the BOJ) to pretty much already be thinking about it,” Salgado said on the idea of tweaking YCC.

{kind=link}