Reuters

As a swift and broad rally in Asian stock markets after China’s reopening from COVID curbs peters out, investors are targeting beaten down stocks in sectors including retail, hospitality and technology to lead a narrower advance from here.

The initial wave of optimism over the lifting of lockdowns in the world’s second-largest economy lifted a host of trade and tourism stocks around the region, led predictably by the most obvious beneficiaries – sectors such as Macau hotels and Thailand tourism.

But three months in, investors reckon it is time to get more discerning.

“We believe the next phase of the market’s recovery will be focused on companies that can deliver resilient earnings growth,” said Robert Secker, portfolio specialist in the equity division at T. Rowe Price.

Herald van der Linde, HSBC’s head of equity strategy for Asia Pacific, points out that travel and gaming stocks have already benefited.

“I think in the remainder of 2023 it is all about how the recovery in China filters through to consumer companies and banks outside of China,” he said.

For investors looking for their next leg of growth, analysts recommend sectors that stand to benefit from the pent-up demand of Chinese consumers, such as hospitality firms, retailers, and industries that struggled during the economic downturn, including online recruiters and shopping mall operators.

Investors are banking that sky-high Chinese household savings, which jumped to 17.8 trillion yuan ($2.62 trillion) last year, will be released and boost these sectors.

Man Wing Chung, lead manager for Value Partners’ Asia ex-Japan Fund is adding to technology hardware and semiconductor stocks in Taiwan, saying their “valuation has already priced in a lot of the negative sentiment on the downward tech cycle.”

While shares of Taiwanese chipmaker TSMC have risen 45% from their October lows, they still trade at 15.5 times forward earnings, below a 5-year average of 18.8 times.

GRAPHIC: TSMC valuation –

Driven by expectations people in the world’s most populous country will rush to travel and socialise after three years of the most stringent pandemic lockdowns, shares of Macau gaming companies Sands China, Wynn Macau, MGM China have all more than doubled in the past three months.

Singapore Airlines is up 12%, while Trip.com Group Ltd has gained 68% in the same period.

China’s market has naturally benefited most, with the MSCI China index up nearly 50% since start of November, far outperforming the 13% rise in the MSCI Southeast Asia index and 26% gain in MSCI’s broad Asia-Pacific index.

That has led investors to hunt for sectors and companies with depressed valuations outside China.

Also, since China accounts for more than 20% of exports from the Association of Southeast Asian Nations, a recovery in China will lift up growth of the entire region, said Value Partners’ Chung, who is overweight on markets in the ASEAN bloc.

Data from stock exchanges in Taiwan, India, the Philippines, Vietnam, Thailand, Indonesia and South Korea shows foreigners purchased $8.8 billion worth of stocks in January, with Taiwan and South Korea witnessing their biggest monthly purchases in at least two years.

Foreign investors had sold $57.2 billion in regional equities last year.

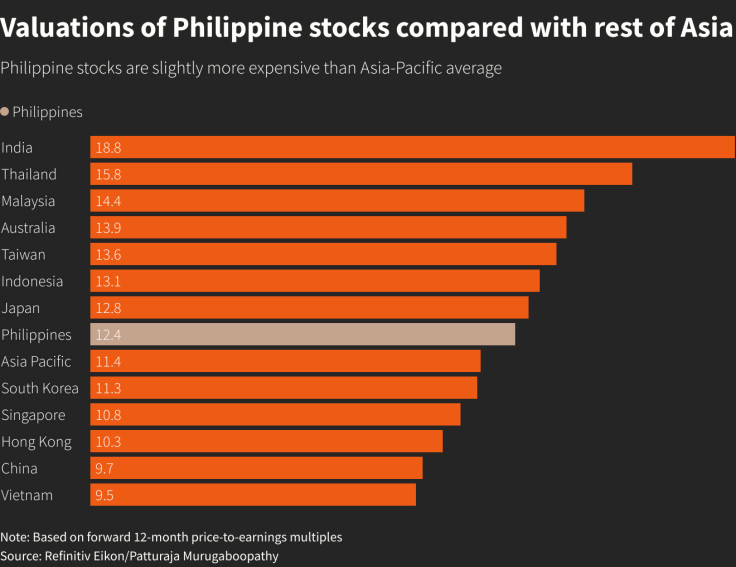

GRAPHIC: Valuations of Philippine stocks compared with rest of Asia –

GRAPHIC: MSCI China outperforms regional –

GLOBAL PUSH OR CHINA PULL?

After a torrid 2022, investors have been betting that a swift recovery in China’s economy will somewhat cushion the impact of a global slowdown and possible recession.

Value Partners’ Chung said the concerns over global recession have been largely priced into the market and the benefits from China reopening have yet to be felt.

With global inflation showings signs of easing and investors expecting major central banks to soon end their monetary tightening, their attention has been switching to the possibilities of a global recession.

“Everyone seems to ‘know’ we’re going to have a recession, and everyone seems to ‘know’ it will be mild,” said Christy Tan, investment strategist at Franklin Templeton Institute.

“China and its reopening trade, on the other hand, are in early stages and may be the additional tailwind for Asian equities later this year.”

($1 = 6.7850 Chinese yuan renminbi)

Reuters

{kind=link}